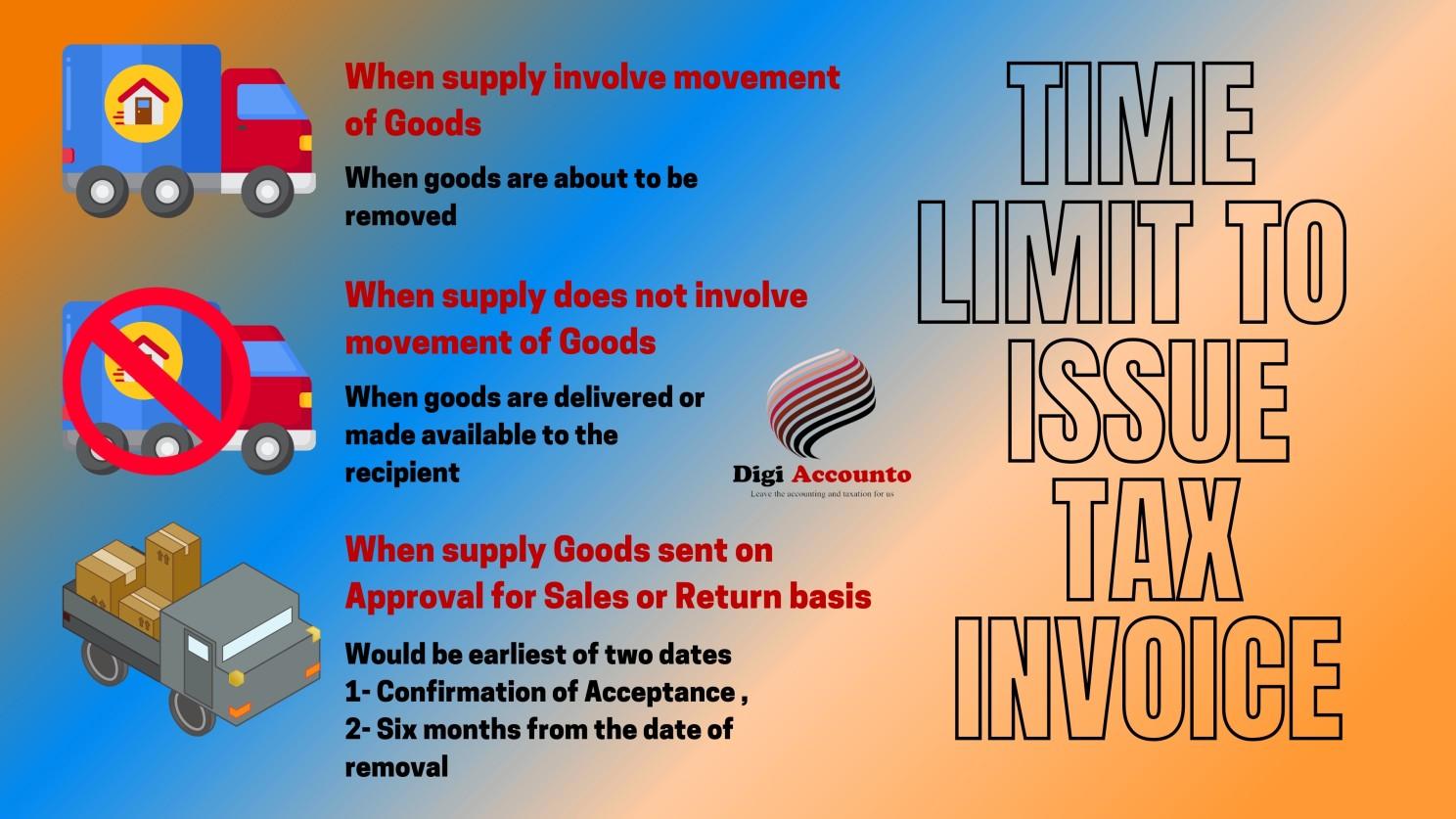

Time of Supply under GST Law | How to Determine Time of Supply Under GST Act | Time of Supply of Goods | Time of Supply | Digi Accounto | Business ATM Services |

Time of Supply under GST Law | How to Determine Time of Supply Under GST Act | Time of Supply of Goods | Time of Supply | Digi Accounto | Business ATM Services |

Time of Supply under GST Law | How to Determine Time of Supply Under GST Act | Time of Supply of Goods | Time of Supply | Digi Accounto | Business ATM Services |

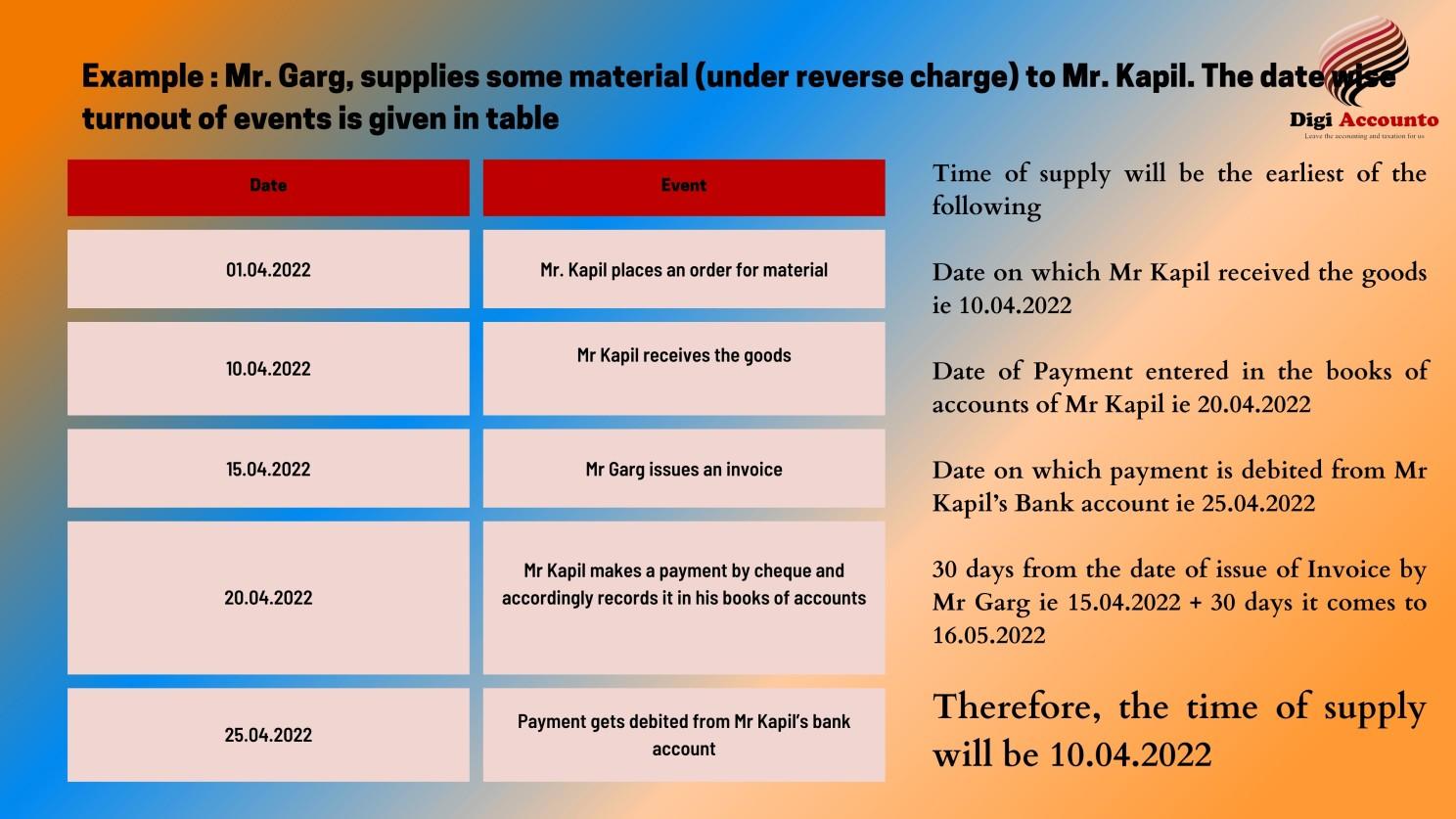

Time of Supply under GST Law | How to Determine Time of Supply Under GST Act | Time of Supply of Goods | Time of Supply | Digi Accounto | Business ATM Services | Time of Supply under Reverse Charge

Time of Supply under GST Law | How to Determine Time of Supply Under GST Act | Time of Supply of Goods | Time of Supply | Digi Accounto | Business ATM Services | Time of Supply under Reverse Charge

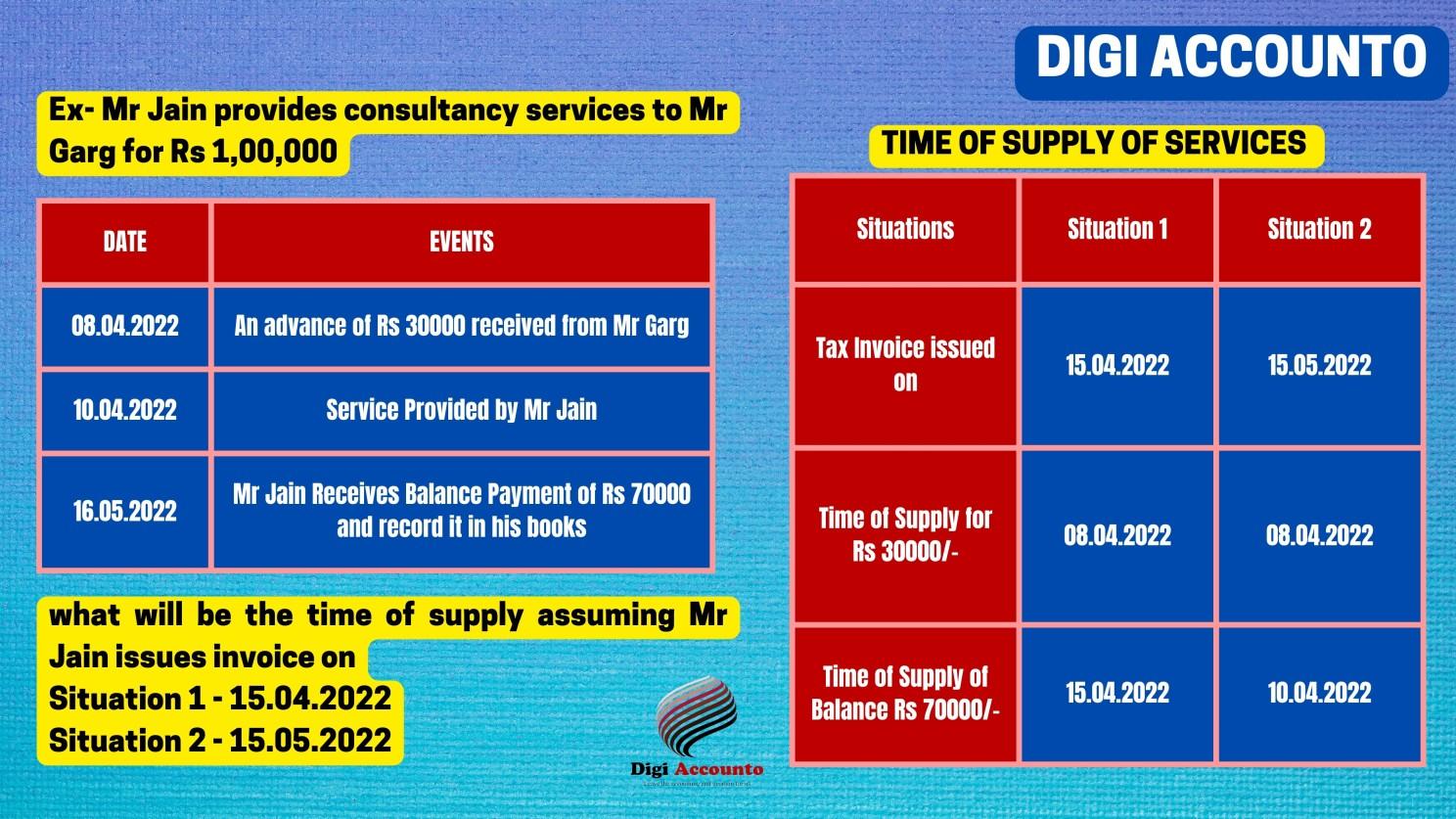

Time of Supply under GST Law | How to Determine Time of Supply Under GST Act | Time of Supply of Goods | Time of Supply | Digi Accounto | Business ATM Services | Time of Supply under Reverse Charge

Time of Supply under GST Law | How to Determine Time of Supply Under GST Act | Time of Supply of Goods | Time of Supply | Digi Accounto | Business ATM Services | Time of Supply under Reverse Charge